The German pension system consists of 3 layers or pillars. The first layer is the state pension. More than 30 million current employees in Germany rely on the pillar of state pension.

In the German system, the current working generation pays the payout of pension for the currently retired citizens with their dues. This model is called the intergenerational contract.

Standard pensions begin at the age of 67, and early retirement from 65 onwards is only possible to a limited extent at costs, causing about a 10 percent deduction from their pension.

Due to the negative demographic development in Germany, the level of pension payouts has shrunk already and will continue to shrink in the coming years. Private and company pension plans are necessary to maintain the standard of living in old age.

With a German pension calculator, you can calculate the gap in your pension and how much you need to provide privately to maintain your standard of living.

Pension system in Germany: Three pillars of pension insurance

The pension system in Germany is based on a three-layer model. It combines the state pension with private or company pension plans. Which of the pillars is relevant for you and which subsidies you receive in the respective models depends largely on your occupational status. The three pillars (or layers) of the German pension system are:

1st pillar

Basic pension including - Statutory pension - Rürup pension - Special pension systems for doctors, lawyers, etc.

2nd pillar

Tax subsidized pension mainly for employees - Company pension - Riester pension

Almost every employee is covered by the first layer. However, due to demographic change, it is already clear today that the statutory pension will not be sufficient to secure the standard of living in old age. At most, it provides a basic subsistence level.

Therefore, additional pension savings in layer 2 and layer 3 are strongly recommended. Which pension scheme is the right one for you depends on whether you are employed or self-employed, whether you want to take advantage of government subsidies or save flexibly, and how much time you have until you reach retirement.

Different forms of flexibility (or lack thereof) are also important. And very important is the question of costs: pensions are sold around the world often still based on commission payments for the advisor, which can lead to very high costs that run counter to your wish to have an efficient savings tool for your pensions. While we can offer commission-based advice on pension plans if you prefer that, we also offer strictly fee-based advice with so-called “Netto-Pläne” for both German pension plans and offshore pension plans alike.

1st Pillar: The statutory / public pension in Germany

When it comes to pensions, more than 30 million employees in Germany rely on the pillar of public pension. The German pension insurance (DRV - Gesetzliche Rentenversicherung) is part of the 1st layer of the German pension system.

It is thus a statutory pension insurance by definition. The DRV was founded in 1891 by the German Reich Chancellor Bismarck, and states that all employees must pay into the DRV. This, btw, also extends since the beginning to some professions that consider themselves to be freelancer, like teachers and trainers.

Other freelance professionals such as doctors or lawyers are usually forced to join their own professional pension funds instead of the DRV. Public servants are not in the DRV; they receive a separate pension from the state.

Every employee in Germany pays directly into the German state/public pension. There is no exemption to that. Whether that is a good deal for you or not will depend on your level of income (i.e. how high an amount is deducted from your gross salary and paid into the public pension). Because the higher your income is, the higher is your contribution – but it is not really likely that you’ll receive an adequate “ROI” for those higher amounts in the long run.

The German public pension system is a social-welfare program where the high-earners subsidize the pensions of the low-earners. At least your employer is contributing half of the monthly contributions.

Cost of public pension: The pension contribution rate is currently 18.6%, half of which is to be paid by the employee and half by the employer. The billing and bank transfers are automatically carried out by the employer.

Pension age and early retirement

Standard pensions begin at the age of 67, and early retirement from 65 onwards is only possible to a limited extent at costs, causing about a 10 percent deduction from their pension. Self-employed persons may become voluntary members. You’ll reach the highest pension possible within the system after 45 years of working in Germany.

How many years do you have to work in Germany to get pension?

Important for Expats: You must have paid in for at least five years (>60 months) to have earned a pension entitlement.

This is often a requirement if you apply for a permanent residence permit, because once you have accumulated those 60+ months (and times in other EU-member state’s pension systems counts toward the 60- months threshold, too), you have an irrefutable right to receive a pension payment from the German pension when you reach retirement age.

With some countries outside the EU there are social security agreements that also need to be checked out for diligent pension planning.

If you have worked in Germany for less than 60 months, when you return to non-European countries, you can demand your own contribution share back from the DRV after two years of leaving Germany. Upon request, we can help you together with our network of professionals.

Why expats trust us

100% English-speaking advisors - "Life is too short to learn German".

Offers from more than 150 insurance companies - with us you really have the choice

Many years of experience and specialisation - we know the needs of expats

Challenges and information on the statutory pension

1. How public pension works and what to expect from this system

No account – no interest rate – no capital formation. The DRV works according to the pay-as-you-go system. Also known as an intergenerational contract, working-generation pension contributions are used to finance the current pensions of the elderly.

First in – first out. The German pension insurance always speaks of a “pension account”. In fact, this account does not contain any capital that is personally allocated to the insured person. Through first in – first out, it is also not possible to create any capital that could bear interest. The DRV may only have a minimum reserve of 1.5 months expenditure in the fund.

The DRV must not accumulate any surplus. Usually there is little risk of that happening, it is most often the federal government that needs to subsidize the pension system with extra amounts.

2. Uncertain future of the state pension: Demographic problems

The DRV’s pay-as-you-go system is economically dependent on the number of contributors and their income. In the past 30 years, pensions in Germany had to be cut mainly because of mass unemployment and the corresponding lack of premium payments.

Also, demographic problems will arise when the last baby boomers retire from around 2025 onwards. There will be significantly more people of retirement age in Germany by 2035. The number of people aged 67 and older will rise by 22 percent between 2020 and 2035 - from 16 million to an expected 20 million, according to the Federal Statistical Office.

In 2020, there have been 57 pensioners for every 100 contributors; in 2030, there are likely to be 67, and in 2050, about 77. Contribution rates will therefore have to rise - or pensioners will have to draw less money. The DRV takes a mixed approach to this situation: contributions will be gradually increased and at the same time pensions will see reductions.

As a result of various pension reforms, the net pension level (supply ratio) has decreased, i.e. the comparison of net pensions to the last working income before retirement.

3. How much money is the average pension in Germany?

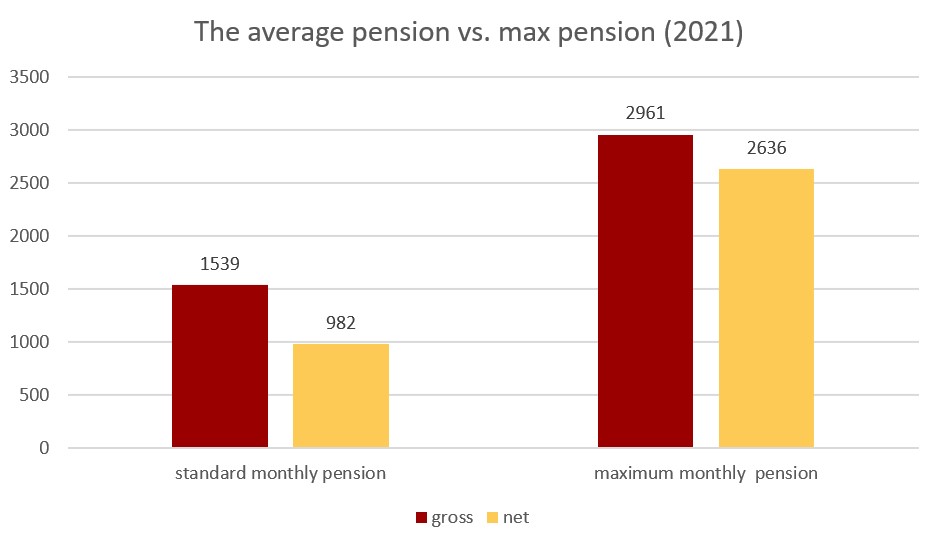

As of July 1, 2021, the standard monthly pension under the statutory pension insurance scheme in the old federal states is set around € 1,539 gross. In the Eastern Germany, it is somewhat lower - there, the standard pension is around € 1,506 gross per month.

How high is the net average pension?

According to this, the average pension payment, i.e. the net amount after deduction of health insurance and long-term care insurance contributions, of all pensions is € 982 net per month. In contrast, pensioners who retired in 2020 only receive € 855 per month. Thus, a quarter of all pensioners who have paid into the pension fund for 40 years receive less than € 1,000 in pension per month.

The average pension amount for public pensions for women in 2018 was approximately € 711, 62 percent of the average pension amount for men. Men receive an average of € 437 more in old-age pensions per month than women.

What is the highest public pension an employee can be obtain with contributions?

Around 25.8 million people receive a pension from the German pension insurance. Deducting orphans' pensions, there are a proud 21.2 million pension recipients as of 2020.

Only a fraction of these receive € 2,000 or more each month: In 2015, there were just 97,271 affected persons. German pension insurance has calculated how high the pension will be in 2022 if a person in the West earned a salary equal to the contribution assessment ceiling in each of his 45 years of work from 1977 to 2021.

The maximum pension in that case is € 2,961.90 gross or € 2,636.09 net.

Pension calculator for Germany: Calculate retirement pension from public pension insurance

How to calculate pension in germany? The calculation of your retirement pension from public pension insurance is not simple. But as soon as you have completed the 60 months of premium payments, you will receive annual information from the Federal Pension Fund.

This annual information shows you your minimum pension entitlement already earned and an estimated pension amount if you continue to pay in at the same level of income until you reach retirement. However, as an expatriate, you can also easily calculate your pension entitlement at 67.

How to calculate my pension in Germany?

Pension calculation is not reducible to a small simple formula. Your monthly pension amount is a multiplication of different values. This is how it works:

Pension formula for the calculation of the pension:

Monthly pension amount = earning points x access factor x current pension value x pension type factor

The formula is not simple. The earning points are the most important value. There is one point per year of employment if your income corresponds to the average income in Germany. If your income is lower than the average, for example, you will receive only 0.9 points, and if your income is higher, you may receive 1.2 points. A maximum of 2 pension points can be achieved per year.

The access factor tells you when you will retire. If you retire at the standard age of 67, this value is 1.0. If you retire early, the value is reduced and you receive a lower pension. The pension value is the equivalent of one earning point. This is always adjusted to the economic situation and increases over time to compensate for inflation.

Last comes the pension type factor. If you work full time until retirement and pay into the pension, this factor has a value of 1.0. It only changes in the event of disability or if you receive a widow's or orphan's pension.

Example of the calculation of the pension for an expatriate If you work in Germany for ten years and always earn the average income (2021: € 41,541), this calculation for the pension results:

You can find the current pension calculator on the official website of the German Pension Insurance (DRV). Unfortunately, the calculator is only available in German there.

Disability pension from the state pension

If you are no longer able to work for health reasons, a pension for full reduction in earning capacity is intended to replace your income. If you can still work a few hours a day, the pension for partial reduction in earning capacity supplements the income you still earn yourself.

Example: you came to Germany at age 32, worked for ten years and earned a gross average income of 4,000 euros. This corresponds to 400 euro pension entitlements. Now you are 42 years old and disabled.

In this case, the DRV will add 20 years or more to your calculation: 400 euros in ten years equals 1,200 euros in 30 years: 1,200 euro monthly pension in case of disability. In most cases, however, only half of this amount is paid because the DRV assumes that you can still work 3–6 hours a day.

This realistically means a disability pension of 600 euros. And a big loss of income. You should, therefore, make sure you set up a decent income protection plan with private insurances for yourself to cover this major risk in your financial planning for the future.

Rürup or basic pension: 1st layer for self-employed

The Rürup pension was set up in order to allow the self-employed a similar pension saving like in the public pension (to which they usually cannot contribute). But high-earning employees and public servants as well as people occupied in special areas like lawyers, architects and doctors, where the guild of their professions offers special pension systems, can use Rürup pension plans to save extra monies into their pension planning with tax subsidies.

One of the main reasons why the Rürup or basic pension counts in the first pillar is that the saved capital cannot be paid out as a lump sum. The Rürup pension can only be paid out as a monthly annuity. This means that it is also vested and protected from the insolvency estate even in the event of insolvency.

The Riester pension was introduced as a state-subsidized retirement provision for employees. With the Riester pension, savers combine their private retirement provision with state allowances. To receive these in full, they must pay four percent of their gross annual income into their Riester contract (but no more than 2,100 euros).

Until December 31, 2021, the Riester was considered by many intermediaries to be the preferred product for private retirement provision. However, due to a change in the actuarial interest rate as of 01.01.2022, this product has moved significantly into the background. You can find out how best to deal with existing Riester contracts and whether a new contract is still worthwhile on the following pages or directly in a personal discussion with our advisors.

The company pension plan is a state-subsidized form of supplementary pension through the employer. There are various models of occupational pension schemes. In the best case, the employer pays all contributions to the company pension plan and the employee benefits from it in retirement.

In the meantime, the more common variant is to split the contributions. Both the employer and the employee pay part of the insurance contribution. The employer's share is at least 15% of the total contribution.

You can find out whether the bAV is worthwhile and what considerations you need to take into account on the following pages or in a conversation with our consultants.

The private pension insurance of the 3rd layer is a supplement to the statutory pension from layer 1 and the subsidized options of layer 2. Only by combining all three layers will it be possible to maintain the standard of living in retirement.

Private pension insurance offers the highest degree of flexibility. Depending on the product, there are also tax advantages. In this case, "not subsidized" simply means that there is no direct state subsidy. However, depending on the choice of insurance model, there is tax relief. Possibilities are for example:

Classic pension insurance Classic annuities are tariffs without a guaranteed interest rate, which invest your savings contributions exclusively in the security assets. By foregoing guarantees, there is a higher surplus participation and the prospect of a higher return. Tariffs with guarantees are no longer very common due to the low expected return.

Unit-linked pension insurance With these products, the savings contributions are invested exclusively in investment funds. The expected return is correspondingly higher than for traditional tariffs.

Defined contribution hybrid pension insurance Hybrid annuity insurance is a mixture of the first two variants. In this model, the customer decides what proportion is invested in the fund and what proportion is invested in the security assets. There is no provision for reallocation by the insurer.

Getting qualified and expert advice for your pension planning

As can be seen from the above, relying only on the public pension in Germany does not lead you to having a sufficient, sustainable income in old age if you want to keep up a good living standard here in Germany.

Therefore, additional savings are strongly recommended. If you like to use tax savings for building up additional pension capital, there are pension schemes available for employees that can make a lot of sense:

Company pensions (bAV – betriebliche Altersvorsorge)

RIESTER pension plans

RÜRUP pension plans

In the end it will always be helpful – especially when you also have pension pots from abroad from the past – to have a financial advisor analyzing with you the pension gap in your financial long-term planning and then setting up a strategy that fits to your personal and financial situation and life-plans like a custom-tailored suit.

And, as you could see above: the public disability pension is not offering you any amount that would make it possible to continue living a normal life at least financially.

Therefore it is very strongly recommended to set up an income protection insurance for everyone in Germany, all the more so if you have dependents that rely on you as the main source of income. There are different ways and means for doing that, some even can be written off against your income and thus reduce the taxes.

But this is definitely not a field for try-and-error as a layman: this is too important to risk making mistakes or overlooking important small print in the coverage, therefore always use a qualified advisor to guide you thru these options in order to find the right one for you.