Occupational pension schemes (bAV) are part of the 2nd pillar of retirement provision in Germany. It is state-subsidized and is often also supported by the employer.

The great advantage of the bAV is the tax effect. The savings contributions flow from gross income directly into the pension. There is no income tax in the savings phase. The pension is not taxed until it is paid out.

Since 2019, employers must pay at least 15% of the savings contribution. This means that the employer is legally guaranteed to make an additional payment into the occupational pension plan.

There are five different forms of occupational pension. The most frequently used variant is direct insurance. In the event of a change of employer, the insurance can usually be transferred. In any case, your contributions are safe.

A company pension scheme (bAV = betriebliche Altersvorsorge in German) is defined in Germany as the building up of a supplementary pension through the employer from contributions of the employer, the employee, or both combined. Around 18 million employees were entitled to a company pension at the end of 2015. It is thus the major supplementary pension scheme in Germany for employees.

It is currently the most attractive option for employees. You have an instant tax benefit because the contributions are being made out of your gross salary. Often employers offer attractive co-payments already and starting 2019 they have to contribute at least 15% of your contributions by law. Since January 2018 you can defer up to 520 EUR per month (i.e. 6,240 EUR per year) from your gross salary into a company pension via a so-called “Direktversicherung bAV”.

How does the company pension scheme work?

A direct pension plan (Direktversicherung bAV) as the most important implementation method is part of the second layer of the German pension system. It is the most common example of occupational pension schemes. There are a number of other options to set up a company pension plan, but for reasons of brevity and clarity we’ll reduce this info to the one most commonly used in Germany by employees.

In Germany, there is a long tradition of providing for retirement with the help of the employer. More than 100 years ago already, the first large companies began saving assets for employees, from which they later received a pension.

Today, employees can defer contributions from their gross salaries and deposit them, for example, into a pension insurance scheme that the employer takes out for them. This offers them a chance to “save” the taxes and social insurance premiums on their contributions to the bAV.

During the savings phase, the contributions thus flow into the pension plan untaxed. In effect the tax payment is just deferred until you reach pension age… but in the meantime you’ll reap in the benefits of extra yield from these saved taxes. This option is not available in the case of private pension provision, e.g. through a share savings plan. You must save out of your taxed net salary without employer subsidies.

Who pays the contributions to the bAV?

The choice of what kind of pension plans can be used often lies with the employer only, i.e. the employer decides what kind of pension plan the employee is allowed to use. Therefore whether pension provision is worthwhile also depends on the employer’s exact form of company pension scheme and whether they participate in the financing of the contributions. In Germany, five implementation channels for company pension schemes are permitted:

Direct insurance

Pension fund type 1

Pension fund type 2

Support fund

Pension commitment

More important than the choice of model is the employer's decision on how to contribute. Possible scenarios are:

1. The employer finances the company pension scheme in full

In the early days of occupational pension provision, the focus was usually on caring for the employees. Today, companies primarily want to retain employees. In any case, the following applies: If the employer pays for the company pension, employees can enjoy this additional remuneration.

Many foreign employers offer such full payments because they are used to it in their home country. This usually adds up to 4% to 10% of the gross salary. German employers are somewhat less willing to co-contribute to the company pension schemes. But due to new legislation starting 2019 they have to co-pay 15% to new pension plans.

2. The employee alone converts part of his or her salary

Since 2002, employees have had a legal right to pay part of their gross wage into a company pension scheme like the Direktversicherung bAV (so-called deferred compensation). The employer must offer such a contract upon request. Generally, the employer hands over investment responsibility to an insurance company.

Due to the tax advantages, a purely employee-financed direct insurance can also be lucrative – however, one must then pay close attention to the costs and should choose either a contract with group discounts of around 50% or a so-called net tariff (in which case you have to pay a fee to the intermediary/consultant for this, which is usually far lower than any commission costs, though).

3. The employer and the employee both pay part of the contributions

It is also conceivable that the employer pays part of the bAV contributions and pays them into the pension insurance together with the employee’s salary. Up to now, employees particularly in collectively agreed companies have benefited from these set-ups.

But, as said above, many foreign employers are used to co-contributing and often offer quite attractive co-contributions. And starting 2019, employers HAVE to co-contribute 15% to the employee’s contributions in general with new pension plans.

Why expats trust us

100% English-speaking advisors - "Life is too short to learn German".

Offers from more than 150 insurance companies - with us you really have the choice

Many years of experience and specialisation - we know the needs of expats

A major disadvantage of the company pension so far has been that a later pension is counted towards the public pension receipts. Those who are dependent on state support in old age would have saved up for nothing. Since 1 January 2018, depositors are able to keep at least € 100 and a maximum of € 200 of their company and Riester pensions. More precisely: Of pensions that exceed € 100, depositors can keep 30 percent and a total of no more than € 200. For low-income earners it is a significant advantage from 2018 onwards.

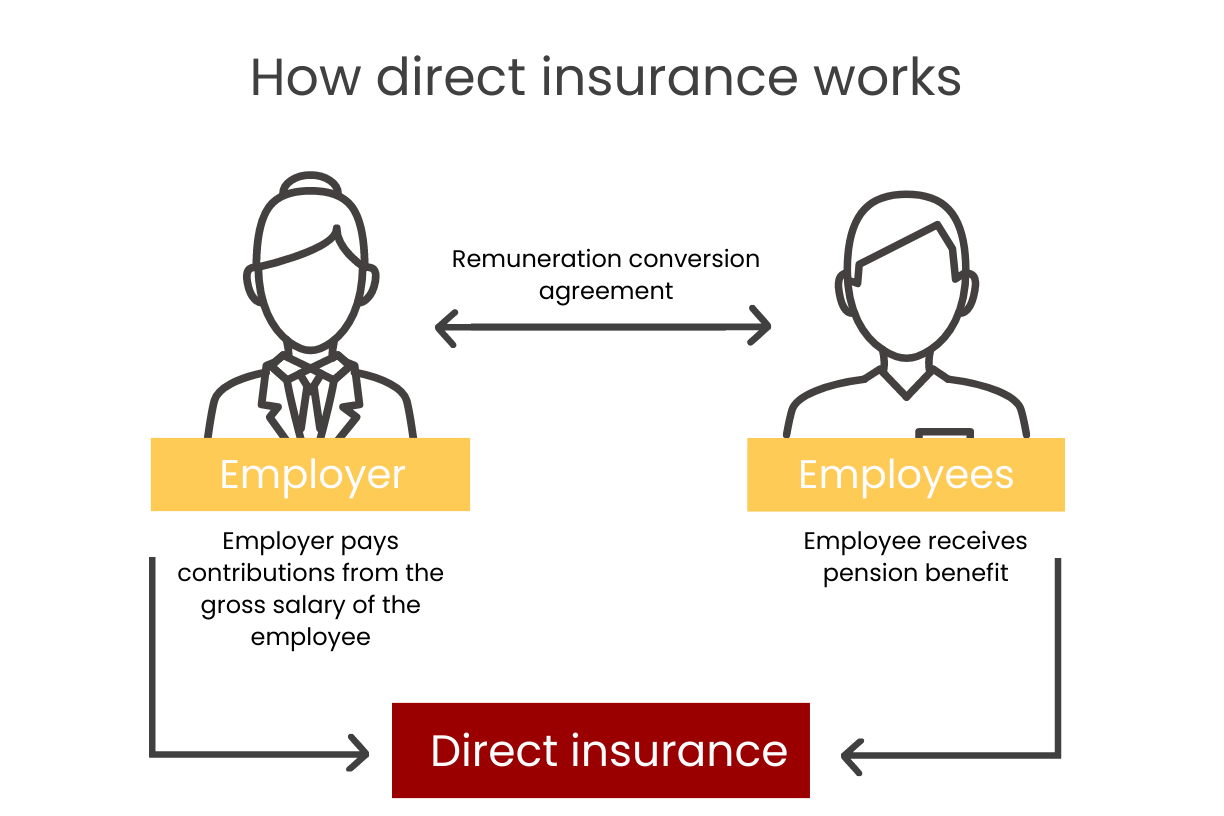

In principle, a Direktversicherung bAV is a private pension insurance policy that is taken out from a life insurer by the employer on behalf of the employee. There are basically no technical differences to private pension insurance.

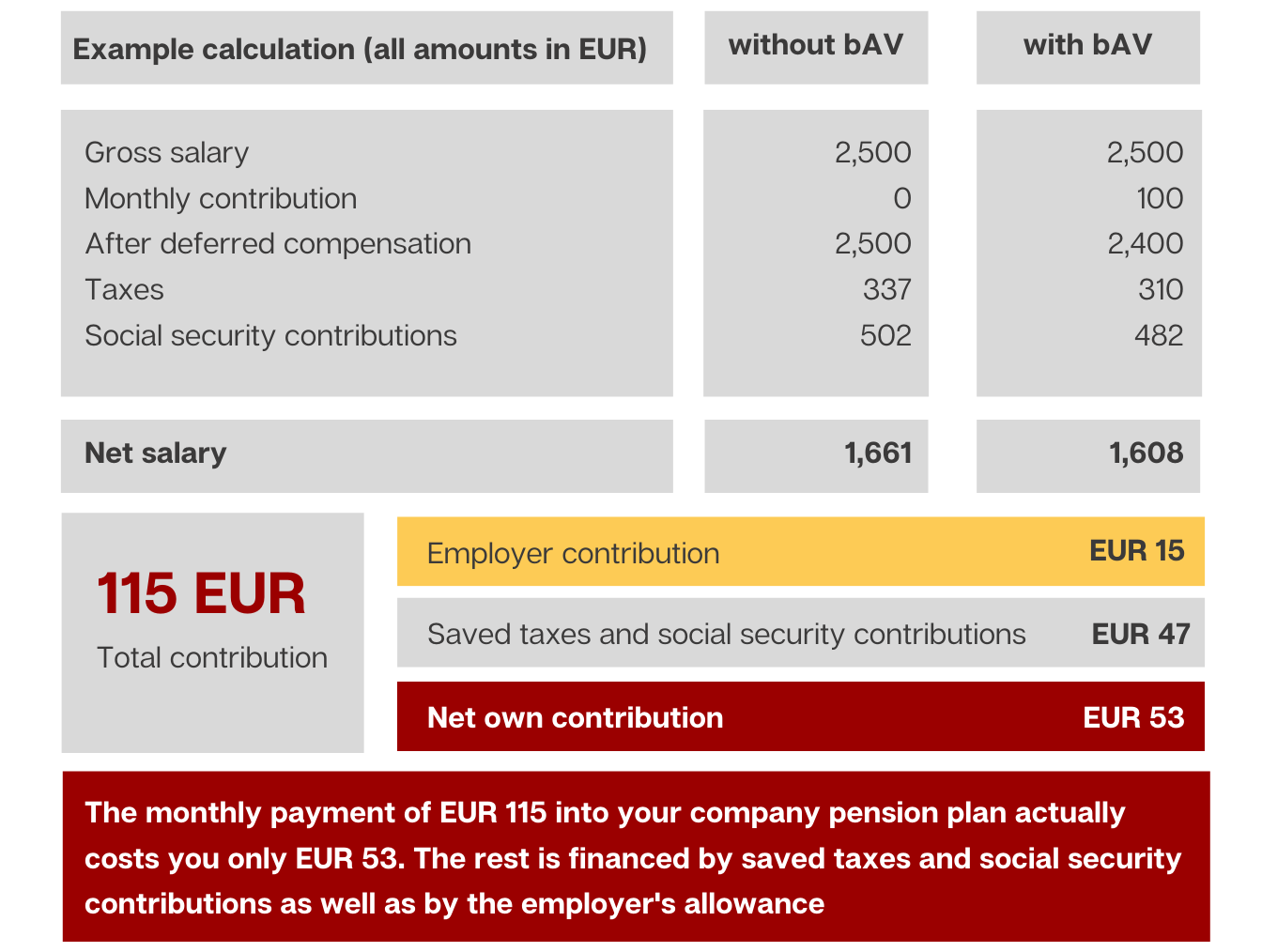

The biggest advantage and special features are tax incentives: Up to about € 520 (value 2018, previously € 260) can be paid into the direct insurance tax free on a monthly basis.

The first € 260 can also be paid free of social security contributions (i.e. pension insurance and unemployment insurance) if your annual gross income is below € 78,000 (2018 status).

Tax and social security savings as well as the employer subsidy make the difference

As said above, a company pension scheme grows the more attractive in Germany if the employer co-contributes AND if the costs of setting up and managing a pension scheme are limited. We at CR&CIE will be happy to work out exactly how this is done in your case.

In the best case, your contribution to direct insurance is subsidized by tax and social security benefits of up to 50 percent. On the other hand, you have to pay full tax on pensions from direct insurance. In Germany, statutorily insured pensioners also have to pay health and nursing care insurance contributions on top of their pensions, which is around 10 percent.

The policyholder of the contract is always the employer. However, there are only formal reasons for this. You as the insured person always have rights of lien. If you change your employer within Germany, you can in most cases “take along” the contract for the new company. Even if that is not the case, you will still receive the pension insurance policy handed out to you – the invested money is yours for your retirement and can’t be taken away from you.

Good to know: There are usually high commissions when taking out direct insurance in Germany. This can be a disadvantage for you if you are staying in Germany for a limited period of time. For this reason, CR&Cie offers direct insurances on request as a fee tariff or, if the employer is involved, as a group tariff with up to 50% lower costs.

Independent advise for expats

Let us help you with your company pension scheme

German pension regulations are complicated and sometimes incomprehensible - typically German! We at CR&Cie have years of experience in advising expats and know exactly what is important. Especially because in many situations up to four different pension models and variants have to be examined.

We are also happy to speak directly with your employer's HR department. We also support employers in introducing a company pension plan in their companies. Give us a call.